Estimated reading time: 7 minutes

June 9, 2026 – How Ransomware Enters Credit Union Networks – by Zach Carothers – in Cybersecurity, Compliance

Ransomware rarely enters a credit union through a direct technical attack on your servers. In most cases it enters through a person. A staff member clicks a convincing email, types credentials into a fake login page, or connects a compromised device to the network. The attacks on Ellafi Federal Credit Union in October 2025 and MetroWest Community Federal Credit Union in March 2026, both attributed to the Akira ransomware group, followed that pattern. Stopping it starts with understanding how ransomware enters a credit union in the first place.

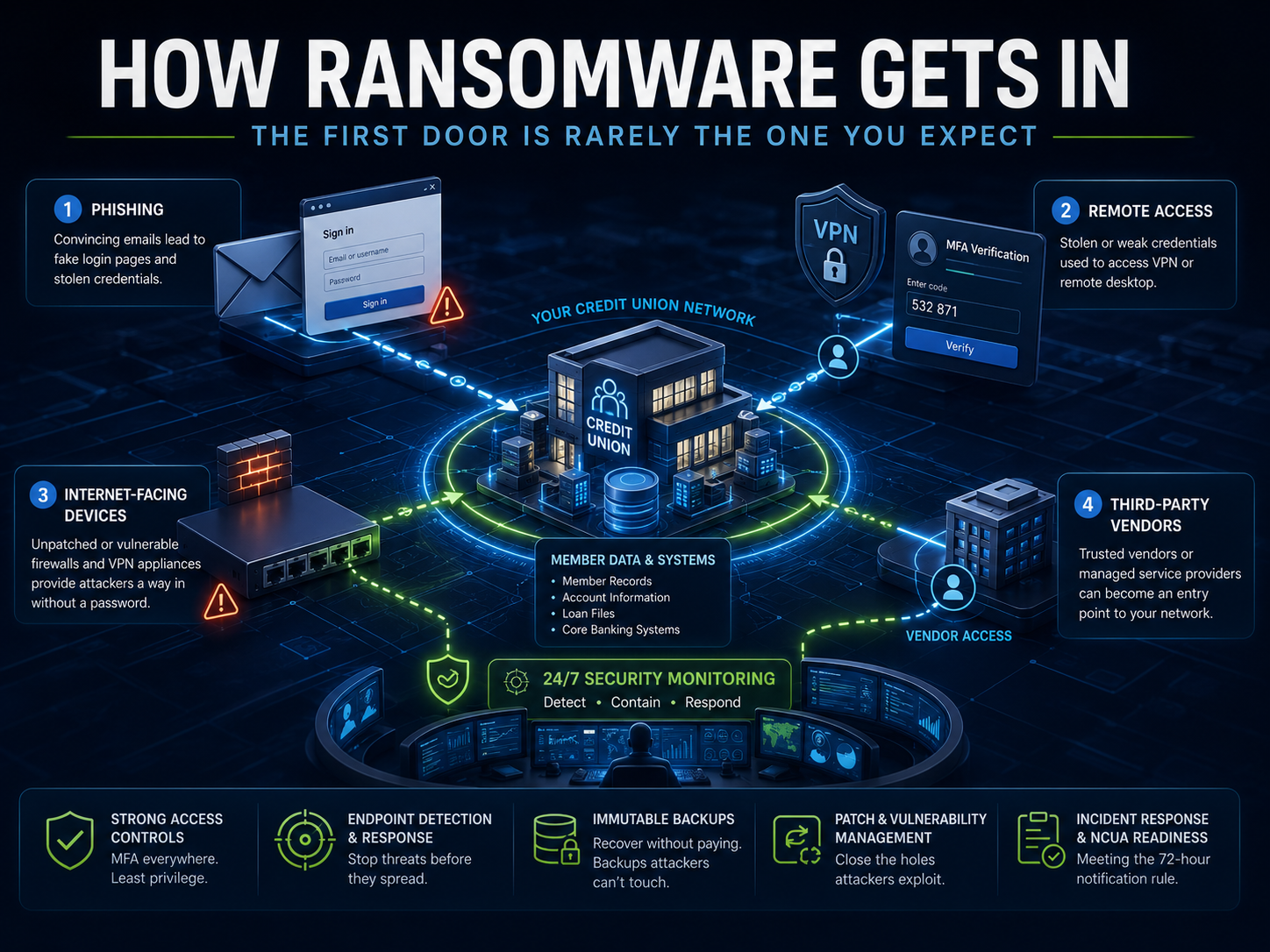

The Most Common Ransomware Entry Points in Credit Unions, Ranked by Frequency

Most credit union ransomware cases begin with one of four entry points.

- Stolen or guessed credentials on remote access. Attackers log into a VPN or remote desktop using a password they bought, phished, or brute-forced. If that gateway lacks multifactor authentication, one working password is enough.

- Phishing and fake login pages. A teller or loan officer receives an email that looks like a vendor, a regulator, or internal IT. The link leads to a page that captures the password, or to a prompt that approves the attacker’s login.

- Unpatched internet-facing devices. Firewalls and VPN appliances with known vulnerabilities give attackers a way in with no password at all.

- Compromised vendors and managed devices. A trusted third party with network access becomes the path, which is why supply chain exposure now sits on every examiner’s checklist.

Notice what is not on that list. Direct assaults on core banking servers are rare. The servers are usually the last stop, not the first. The first stop is almost always an identity or a remote door.

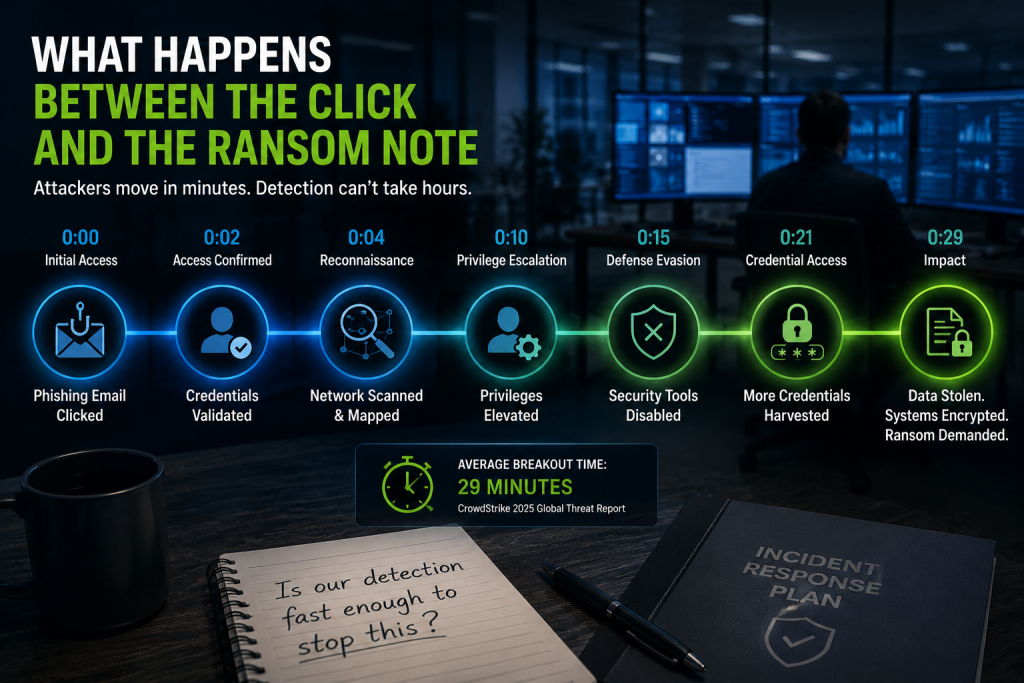

What Happens Between the Click and the Ransom Note

Speed is the part most boards underestimate. CrowdStrike’s 2025 Global Threat Report measured the average eCrime breakout time, the gap between the first compromise and the first lateral move, at 29 minutes. The year before it was 48 minutes. The fastest case on record was 27 seconds.

The sequence inside that window is consistent. An attacker confirms the stolen access and they scan the network to find domain controllers, file shares, and backups. They escalate to an administrator account. They disable security tools and delete or encrypt the backups. Then they deploy the ransomware and post stolen data to a leak site to pressure payment. For a credit union, member records and the core system can be encrypted and stolen before anyone has acknowledged the first alert. Detection that takes hours cannot beat an attack that moves in minutes, which is why monitoring has to run around the clock with a response measured in minutes.

Why Smaller Credit Unions Are Disproportionately Targeted

Attackers do not skip small institutions. They prefer them. A credit union under $500 million in assets holds the same valuable data as a large bank: Social Security numbers, account numbers, loan files, and member identities. It usually runs that data with a fraction of the security staff. Akira and similar groups automate their scanning, so they find the weakest exposed device regardless of institution size. One unpatched VPN looks identical to an attacker’s scanner whether it serves 5,000 members or 500,000. The result is a hard mismatch. Small credit unions carry big-bank data with small-shop defenses, and the attackers know it.

How the Akira Group Operates: What the 2025 and 2026 Attacks Revealed

Akira is one of the most active ransomware groups targeting financial institutions, and its methods are documented. According to a joint CISA advisory, Akira gains initial access mainly through VPNs that lack multifactor authentication, using stolen credentials or known vulnerabilities in Cisco and, since July 2025, SonicWall SSL VPN devices, including CVE-2024-40766. Once inside, the group maps the network with common scanning tools, harvests more credentials with techniques like Kerberoasting and pass-the-hash, and moves across the network over remote desktop. Then it runs double extortion: encrypt the systems and threaten to publish the stolen data.

The attacks on Ellafi Federal Credit Union, which exposed more than 17,000 members, and on MetroWest Community Federal Credit Union were both attributed to Akira. The lesson for every other credit union is direct. Akira’s entry point of choice is remote access without strong MFA. Close that door and you, at least, remove the group’s favorite way in.

What “Immutable Backups” Actually Means, and Why They Decide Whether You Pay

A backup only helps if the attacker cannot reach it. Akira and groups like it hunt for backups first and delete them, because a credit union that can restore does not need to pay. An immutable backup removes that option. Immutable means write once, then locked. The data cannot be altered or deleted for a set retention period, even by an administrator account. Paired with an offline or isolated copy, it gives you a clean restore point the attacker cannot touch. Cyber insurers now ask for immutable, tested backups by name, but the real reason to have them is simpler. They are how you say no to the ransom. For a credit union, that is the difference between a bad week and a member-notification event with regulators watching.

The NCUA’s 72-Hour Notification Rule: What a Ransomware Incident Triggers

A ransomware attack is not only a technical event. For a federally insured credit union, it starts a regulatory clock. Since September 1, 2023, the NCUA requires a credit union to report a substantial cyber incident within 72 hours of reasonably believing one occurred. That includes a ransomware attack, a breach of member data, or a serious disruption of operations. The window is short, and it runs whether or not your team has finished the investigation. A documented incident response plan matters as much as the technology here. When an attack hits, you need to know who declares the incident, who contacts the NCUA, and where the evidence lives. A credit union that improvises the 72-hour response under pressure tends to miss the deadline or misstate the facts, and both create a second problem on top of the breach.

What Defensible Protection Looks Like for a Credit Union Under $500M in Assets

Defensible does not mean expensive. It means the controls are real, layered, and provable. Each one below shuts down a specific step in the entry chain.

- Multifactor authentication on every remote entry point, email account, and administrator login, phishing-resistant where possible. This closes the door Akira uses most.

- Endpoint detection and response on every device, monitored around the clock, so a single compromised laptop is contained before the 29-minute breakout.

- Immutable, offline backups with restores tested on a schedule, not assumed. This is what lets you refuse the ransom.

- Patching for internet-facing firewalls and VPN appliances within days, not quarters. This removes the no-password way in.

- DMARC email protection to cut the phishing that starts most attacks.

- A written incident response plan mapped to the NCUA 72-hour rule and rehearsed with a tabletop exercise.

- Vendor oversight, so a third party’s weak control does not become your breach.

Read together, these turn the attack chain into a series of stops. The attacker who lands on one phished credential never reaches the backups.

Most credit unions under $500 million cannot staff a 24/7 security operation in house, and they do not need to. What they need is a partner who watches the network every hour, contains the first compromised device before it becomes a breakout, and has the response steps ready for the NCUA’s 72-hour clock.

TorchLight Secured & Managed IT has protected regulated institutions for nearly two decades, with a 30-minute critical first response, 24/7/365, documented incident response your examiners can follow, and a 100 percent regulatory exam pass rate for clients at full program maturity. If your remote access, your backups, or your response plan would not hold up to the entry chain above, start with a TorchLight managed security assessment.

TorchLight specializes in managed security services for organizations where security and compliance are non-negotiable. With 18+ years serving regulated industries, 24/7 SOC operations, and deep regulatory fluency across GLBA, HIPAA, and SEC requirements, TorchLight delivers security operations leadership can defend.

Ready to explore what partnership looks like? Schedule a consultation to discuss your organization’s specific security needs and regulatory requirements.